Blog

FintechZoom.com Lifestyle Guide to Smarter Modern Living

Most of us still manage our lives the same way we did ten years ago. We stress about bills, forget to invest, overpay for things we barely use, and somehow always feel like we’re playing catch-up. Sound familiar.

That’s exactly where the FintechZoom.com lifestyle comes in. It’s not a luxury club for wealthy investors or a tech manual that only engineers can follow. It’s a practical, everyday approach to living smarter using digital tools, financial habits, and real insights that anyone with a smartphone can access today.

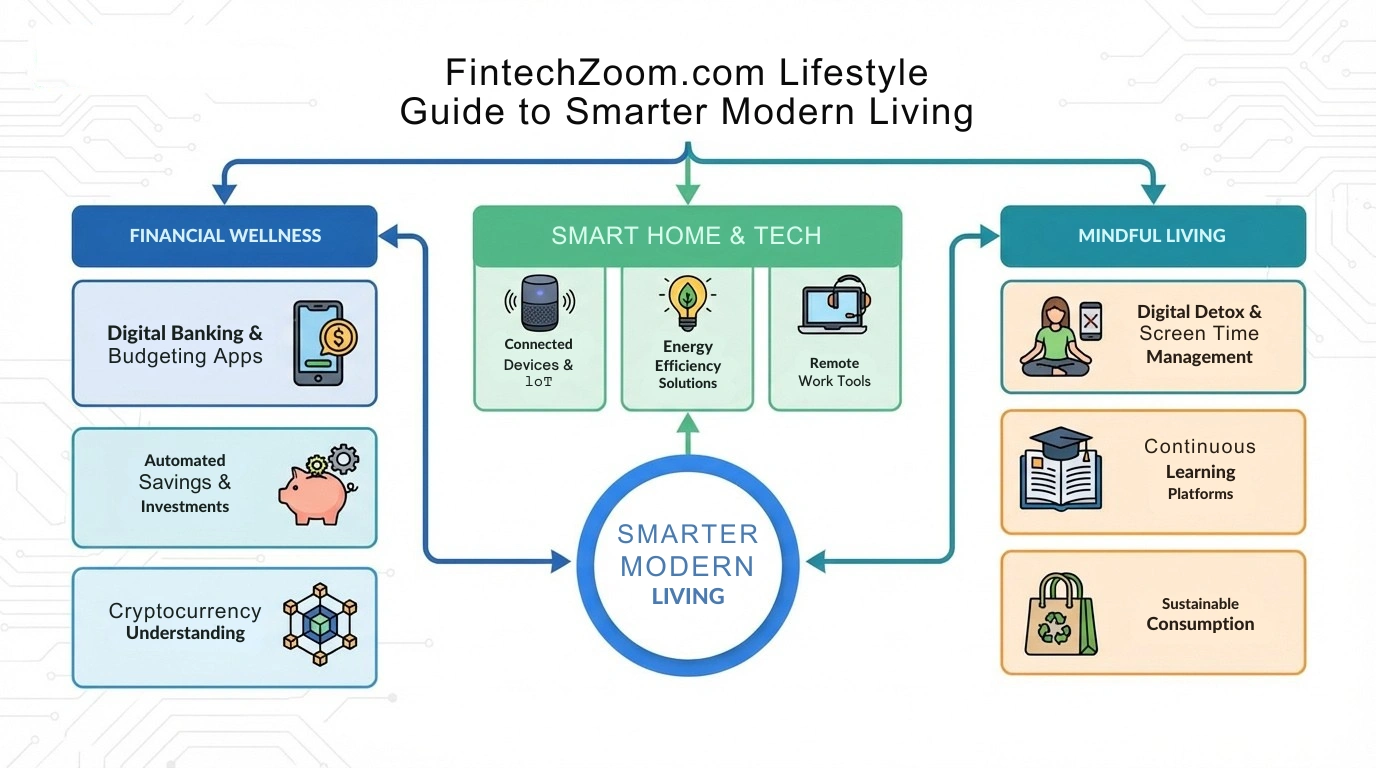

What Is the FintechZoom.com Lifestyle?

The FintechZoom.com lifestyle isn’t a brand you pay for. It’s a mindset a way of combining financial technology, smart daily habits, and modern tools to improve the quality of your everyday life.

Think of it as three things working together:

- Money intelligence — knowing where your money goes and making it work harder for you

- Technology fluency — using the right digital tools without feeling overwhelmed

- Intentional living — making conscious choices about your time, spending, and priorities

When these three work together, you stop reacting to life and start shaping it.

Building a Smarter Financial Foundation

A solid financial base is where everything starts. The good news is you don’t need to be a finance expert or earn a big salary to build one. You just need the right tools and a few habits you actually stick to.

Start with automated savings. Apps like Digit, Qapital, or the round-up feature inside most modern living banking apps move small amounts into savings on their own. You set it up once and it runs without you touching it again.

Get clear on where your money actually goes. Apps like YNAB or Copilot show your real-time spending in a way that most people find eye-opening. That awareness alone often changes behavior without any extra willpower needed.

Then start investing, even with tiny amounts. The biggest investing mistake isn’t picking the wrong stock it’s waiting too long to start. Here’s what to focus on:

- Open an investment account with as little as $1 on platforms like Acorns or Fidelity

- Set up automatic monthly contributions, no matter how small they are

- Choose low-fee index funds to begin they outperform most actively managed funds over time

- Turn on automatic dividend reinvestment so compounding works in your favor

Credit Score Management as a Daily Lifestyle Habit

Your credit score affects your life quietly but constantly. It shapes your mortgage rate, your car insurance premium, rental approvals, and sometimes even job decisions. Yet most people only check it once a year usually after something has gone wrong.

The FintechZoom.com lifestyle treats credit management as an ongoing habit, not a panic reaction. Free apps like Credit Karma, Experian, and CreditWise from Capital One show your score in real time and flag changes automatically.

Here are the habits that actually move the needle:

- Pay every bill on time this is the single biggest factor in your credit score

- Set up autopay for at least the minimum on every account so you never miss a due date

- Keep your credit use below 30% of your total available limit

- Don’t open multiple new credit accounts within a short window of time

- Use Experian Boost or UltraFICO to add utility and streaming payments to your credit history

That last point is worth noting. If you’ve paid your electricity, phone, and streaming bills on time for years but have a thin credit file, these tools can lift your score in weeks rather than months.

Smart Technology Habits That Actually Improve Your Day

Technology is meant to make life easier. But let’s be honest most of us use it in ways that leave us more distracted, not less. The smart approach here is to be intentional. Use tech where it genuinely helps, and cut it where it doesn’t.

Digital wallets like Apple Pay and Google Pay don’t just speed up checkout. They log every purchase automatically for expense tracking, so you always know what you spent and where.

Smart home tools like Nest or Ecobee thermostats can reduce energy bills by 10 to 15 percent a year with no ongoing effort. Set your schedule once and let it run.

Subscription management is where most people quietly lose money. The average person pays for 12 subscriptions but actively uses fewer than five. Here’s how to fix that:

- Use Rocket Money or Trim to scan all your recurring charges automatically

- Cancel anything you haven’t used in the past 30 days

- Use apps like Billshark to negotiate lower rates on internet, insurance, and phone bills

- Set a calendar reminder every six months to run through your subscriptions again

AI Financial Coaching Your 24/7 Money Mentor

This is one of the biggest shifts in personal finance over the last two years, and none of the top competitors mention it. That’s a real gap, because this changes the game for anyone who can’t afford a traditional financial advisor.

A good financial advisor charges $200 to $400 per hour and usually won’t take you as a client unless you have at least $250,000 to invest. AI coaching tools are filling that gap, and they’re doing it well.

Here’s what these tools can actually do for you:

- Look at your full financial picture income, spending, debt, savings, and investments together

- Give you specific, personalized suggestions rather than generic “save more” advice

- Catch unusual spending patterns before they turn into bigger problems

- Answer any money question you have, at any time, without judgment

- Track progress across multiple goals at the same time

Tools worth trying include Cleo, Monarch Money’s AI assistant, and Bank of America’s Erica. Several major banks expanded their in-app AI features significantly in 2025 and 2026, so check what your own bank already offers.

Use AI coaching as a thinking partner. Let it surface the insights, ask it direct questions about your finances, then make your own calls from there.

Social Fintech and Community Wealth Building

Money used to be a topic people avoided in conversation. That’s changing fast, and the tools making it happen are worth knowing about.

Group savings apps like Tandas and SaveWithFriends let people pool savings toward shared or individual goals. The psychology behind them is solid people stick to savings goals far more consistently when a trusted group can see them.

Social investing platforms like Public.com combine real brokerage features with a community feed where people share their portfolios and reasoning. Used thoughtfully, these communities teach you more about investing than hours of solo reading.

Here’s what social fintech brings to the table:

- Peer accountability makes you far more likely to follow through on financial goals

- Shared investment communities show you strategies you’d never find on your own

- Group savings tools reduce the isolation that makes financial discipline hard to maintain

- Apps like Greenlight and Copper teach kids real money habits through hands-on practice

- Family budgeting apps like Honeydue keep couples on the same page without constant money talks

Sharing a goal with even one trusted person with or without an app significantly increases your chances of reaching it. Research backs this up clearly.

Health, Wellness, and the Money Connection

Your physical and mental health has a direct impact on your finances. Financial stress drives anxiety, poor sleep, and lower productivity. When your productivity drops, your income potential follows right along with it.

The FintechZoom.com lifestyle treats wellness as a financial decision, not just a personal one.

Here’s where health and money meet in practical terms:

- Many health insurers offer discounts or cashback when you hit activity targets through Apple Watch, Fitbit, or Garmin

- Mental health apps like Calm and Headspace reduce stress-driven impulse spending this is a documented, real-world financial benefit

- Meal planning apps like Mealime cut grocery spending and food waste by 20 to 30 percent for most households

- Preventive health habits reduce long-term medical costs, one of the biggest financial threats to middle-income families

- HSA contributions are triple-tax-advantaged pre-tax contributions, tax-free growth, and tax-free withdrawals for medical expenses — yet most people ignore this account entirely

Managing Side Hustle Income the Smart Way

Around 36 percent of American workers now report having some form of side income. Yet almost no lifestyle guide tells you what to actually do with it. Whether you freelance, sell online, drive for a rideshare platform, or do consulting work on the side, your finances are more complex than a standard employee’s.

Here’s the essential side hustle financial checklist:

- Open a separate bank account for your side income from day one this single step makes everything else far simpler

- Track all business expenses like software, equipment, and home office costs because they’re tax-deductible

- Pay quarterly estimated taxes to avoid a painful April bill QuickBooks Self-Employed calculates this automatically

- Keep records of every invoice and payment, even for informal or one-off work

- Open a SEP-IRA if you’re self-employed you can contribute up to 25 percent of your net income, up to $69,000 in 2025, making it one of the most powerful retirement savings tools out there

Most people who qualify for a SEP-IRA have never heard of it. If you earn any self-employment income, this is worth looking into right now.

Travel Smarter Without Spending More

The gap between what smart travelers pay and what everyone else pays is huge. Two people can take the exact same trip and one pays twice as much just because they didn’t use the right tools.

Here’s the FintechZoom.com approach to smarter travel:

- Use travel rewards credit cards like Chase Sapphire Preferred or Amex Gold to earn points on spending you’re already doing

- Book domestic flights 6 to 8 weeks ahead and international flights 3 to 6 months ahead for the lowest prices

- Set up price alerts on Google Flights or Hopper for your specific routes

- Leave on a Tuesday or Wednesday instead of a Friday or Sunday fares drop by 20 to 40 percent just from that one shift

- Look into digital nomad visas if you work remotely countries like Portugal, Estonia, and Costa Rica offer them, and living in a lower-cost country while earning a US salary builds wealth much faster

When you combine reward points, flexible dates, and off-peak destinations, international travel for very little money is genuinely possible. It’s not a myth.

Sustainable Living That Actually Saves You Money

Here’s something worth knowing: the choices that are better for the environment are very often better for your wallet too. Sustainability and smart finances point in the same direction more often than people realize.

Here’s where eco-conscious habits save real money:

- Smart thermostats like Nest or Ecobee reduce energy bills by 10 to 15 percent every year

- LED lighting uses 75 percent less energy than traditional bulbs and lasts years longer

- Buying fewer, higher-quality items reduces replacement costs and waste at the same time

- Solar panels typically pay back their cost within 6 to 10 years and increase your home’s value

- ESG investing lets you put money into companies that match your values and these funds have performed competitively with traditional portfolios

Buying less, buying better that’s one of the most underrated financial principles around. One well-made item that lasts ten years beats three cheap replacements every time, for your budget and for the planet.

The FintechZoom.com Lifestyle Across Different Life Stages

This lifestyle doesn’t look the same at every age, and that’s the point. Where you are in life should shape how you apply these tools and habits.

In Your 20s:

- Open a Roth IRA as early as you can time is the biggest advantage you have

- Build an emergency fund of 3 to 6 months of living expenses before anything else

- Use a budgeting app to build spending awareness while your income is still growing

In Your 30s:

- Automate your mortgage, investments, and insurance payments as much as possible

- Talk to a fee-only financial advisor if your situation gets more complex

- Check your insurance coverage most people in their 30s are seriously underinsured

In Your 40s:

- Max out your 401(k) contributions, especially if your employer matches

- Rebalance your investments to match where you actually are in life now

- Consider real estate as a way to diversify your wealth

As a Family:

- Use shared budgeting apps like Honeydue to stay financially aligned with your partner

- Introduce kids to money early with apps like Greenlight or Copper

- Automate both retirement savings and a 529 education plan at the same time

Avoiding the Common Pitfalls of Digital Financial Living

The fintech lifestyle comes with real risks, and being honest about them is part of using it well.

Watch out for these common traps:

- Over-automation — set a monthly 30-minute check-in to look at your numbers manually and make sure everything is actually working

- Subscription creep — review all recurring charges every six months without skipping it

- BNPL overuse — using multiple Buy Now Pay Later services at once creates debt that’s easy to lose track of

- Blind app trust — only use financial apps from regulated, well-reviewed providers with strong security records

- Weak account security — turn on two-factor authentication for every financial account and use a password manager like 1Password

Knowing these traps exist gets you halfway there. Building the habit of regular review gets you the rest of the way.

Final Thoughts

The FintechZoom.com lifestyle isn’t about becoming a finance expert or turning your life into a spreadsheet. It’s about small, steady upgrades one smarter app, one better habit, one more informed decision at a time. The tools are out there, they’re more accessible than ever, and most of them cost nothing to get started with. Pick one thing from this guide and do it today. That’s genuinely all it takes to begin living a little smarter than yesterday.